Dr. Jürgen Grossmann, Owner, Georgsmarienhütte Holding GmbH / Board Member, DJW

The article is based on a manuscript for a DJW Asa no Kai in Hamburg on December 4th, 2017.

So 04.02.2018, 08:30 Uhr

In the 2009 general election the first Merkel- / SPD “grand coalition” was voted out of office and replaced by a CDU / FDP coalition. On 28th October 2010 the new government used its majority to adopt the extension of the existence of German nuclear power stations by seven and/or 14 years, as they had already announced in their electoral campaign. The main reasons for this were the climate protection targets as well as the reliable and cheap power supply for industry and the population. The energy concept of the new government thus involved the extended use of the nuclear power stations practically as a bridge into the world of renewable energy. Then came the tsunami caused by a seaquake off the coast of Japan, which represented a major catastrophe - most particularly for your country - and for which still today I would also like to express my deep regret and heartfelt sympathy.

The horror of the German public concerning the accident in Fukushima nuclear power plant was enormous and was ultimately responsible for terminating nuclear power in Germany once and for all. Whereas after Chernobyl supporters of nuclear power were still able to argue that Soviet safety standards did not correspond to the level in the west, this argument could not be used with regard to Japan, which is very much respected for its advanced technologies. Even the argument that the event which caused the disaster, the tsunami, could not occur in Germany, was not strong enough to influence public opinion.

After Fukushima the CDU/CSU and FDP also revised their attitudes in favour of an earlier phasing out, which led to the passing of the Act governing the phasing out of nuclear power in spring. The resolution stipulates the precise date of closure for each individual nuclear power station and, according to this schedule, the last nuclear power station will close down in 2022. In chart 2 the temporal development of the nuclear policy in Germany since 2000 is once again presented in summarised form. So you see, particularly in recent years, nuclear energy policy in Germany has fluctuated considerably, with fairly unpredictable economic effects on the energy industry.

The basis for the phase-out decision in 2011 was the work of a so-called Ethics Commission, consisting of 17 persons. Following a two-month period of consultations, they issued a recommendation that the phasing out of nuclear energy would be perfectly feasible from a technical, operational and economic point of view - and that, from an ethical point of view, it was absolutely imperative. This is - albeit abbreviated and expressed rather pointedly - the result of the work of the Ethics Commission which, in my opinion does not even begin to give appropriate consideration to the extensive consequences such a recommendation has for the integrated industrial location of Germany in the heart of Europe.

This statement is confirmed by the situation we actually have in 2017, if we objectively analyse the "successes" so far achieved as a result of the energy transition. The energy transition is currently in an impasse and can no longer be described as a model for success, as the German government continue to present it. The discussion concerning energy policy is to a very great extent guided by ideology, with the consequence that facts are no longer taken into account, or at least are interpreted to match the ideology. I would like to explain these statements, which deviate considerably from the official position of the German government, as I continue with my speech on the basis of the energy policy objectives of the German government, which they would like to achieve with the implementation of the energy transition.

- Withdrawal from nuclear power by 2022.

- Reduction of the CO2 emissions by 2020 by 40% compared to 1990, and by 95% by 2050.

- An increase in power generation by regenerative energy sources by 2030 to at least 50%, and by 2050 to at least 80%, combined with complete electrification of the entire economy, including the mobility and heating sectors.

- Reduction of the total end energy demand in all buildings, also including existing buildings by 60% until 2050.

In the evaluation I would like to orientate myself according to the generally recognised points of the target triangle of the energy policy, which are as follows:

- reliability of supply

- economic efficiency and

- environmental compatibility

Reliable supplies and competitive electricity prices

For a modern, integrated and export-orientated industrial country like Germany, the reliability of the electricity and energy supplies at competitive prices is an absolute necessity. Over recent years a considerable capacity of fluctuating power generation has been developedToday around 100,000 MW are installed in PV systems and wind farms in Germany, but they are not efficiently integrated in the energy system.

Today's power supply is determined and influenced to a great extent by the compulsory input of fluctuating electricity generation from photovoltaic systems and wind farms, which consequently has a significant influence on the grid operation. The increasing stress situations in the German integrated grid is documented by a 10-fold increase of the necessary investments within the last five years. This situation also significantly increases the blackout risk in the German and European grid system. Reliability of supply in the electricity context means that the customer is supplied every single millisecond with high quality electric power - which therefore means sufficient power plant output is an essential requirement.

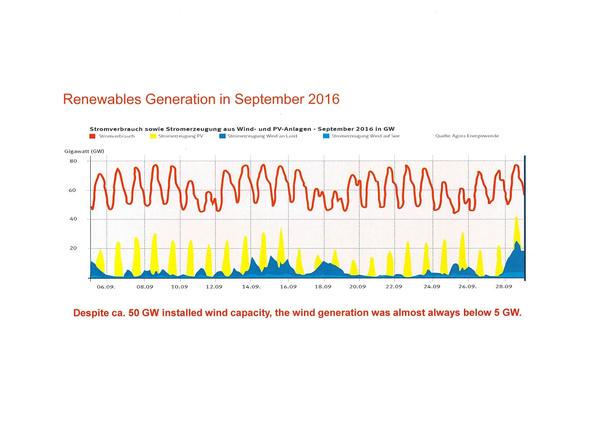

In it becomes clear that, despite the high installed output from photovoltaic systems and wind farms, considerable output from conventional power stations is nevertheless still required (see chart 3). This is actually perfectly obvious because - even in times of the energy transition - the sun still sets in the evening, and the average availability of wind farm output is approximately 2,500 hours per annum. Today in Germany, therefore, a power plant park with an output of over 200,000 MW, has a peak load of just over 80,000 MW. In the liberalised European electricity market, however, this leads to some ridiculous results.

In the liberalised electricity market, in connection with the compulsory obligation to feed in energy generated on a renewable basis, this means that whenever the sun shines or the wind blows, the conventional power stations have to reduce their output to a minimum, as is necessary to maintain a reliable supply. This means that in the case of low demand for electricity, and a good supply of energy generated by sun and wind, electricity has a negative price on the energy exchange - so it can no longer be sold. The price for electricity on the energy exchange is currently in the area of 30 €/MWh, which means for conventional power stations that in many cases they can no longer be operated on an economical basis, and the operators want to close them down. The authorisation for closure is issued by the German Federal Network Agency, which investigates the extent to which the power stations are economically necessary for the generation of electricity. If the result is positive, the power station must remain in operation, naturally financed by a state-stipulated take over of costs, reflected in the electricity prices. This situation also leads to a delay in many new construction projects, which can also have a negative effect on reliability of supplies in future, however.

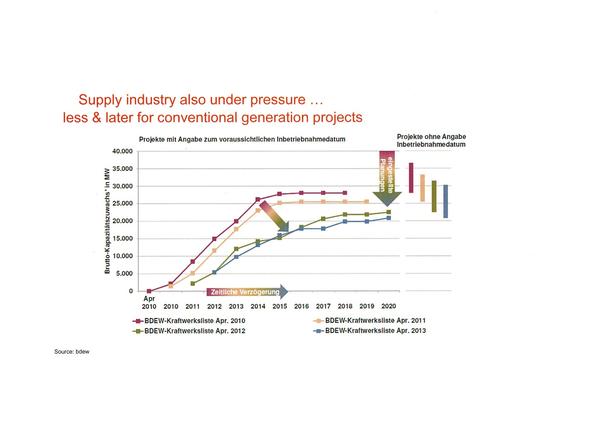

In chart 4 it can be seen that a constantly increasing number of power station projects are delayed, or indeed are relinquished completely. This situation of course has considerably negative economic effects on the energy businesses which own the power stations, and means they can no longer operate them on a profitable basis. Thus the market capitalisation of the two largest German electricity utility companies, RWE and EON was reduced by around 85% between 2007 and 2017, with all the negative effects which such a development involves.

Conversely, the electricity prices for consumers are meanwhile the highest ever recorded. A household customer in Germany nowadays pays an average of 29.6 €Cent per kWh (chart 5), an average industrial customer pays 15- 20 €Cent per kWh, depending on purchasing structure. In Sweden electricity prices for the same industrial customer are just under 7 €Cent per kWh. And indeed, compared to other competitive countries such as the USA, Russia or China, the difference is even greater. The negative effects which this development has on Germany as an industrial location can be measured by the fact that the net investment quota is negative, i.e. the depreciations are higher than the new investments.

At this point it is always pointed out to the general public that Germany is economically very strong, and such prophesies of doom are thus out of place. The process of industry relocating to other, more favourable, countries is a gradual one however, and not instantly visible. And there is one other important point to consider, which I would also like to mention.

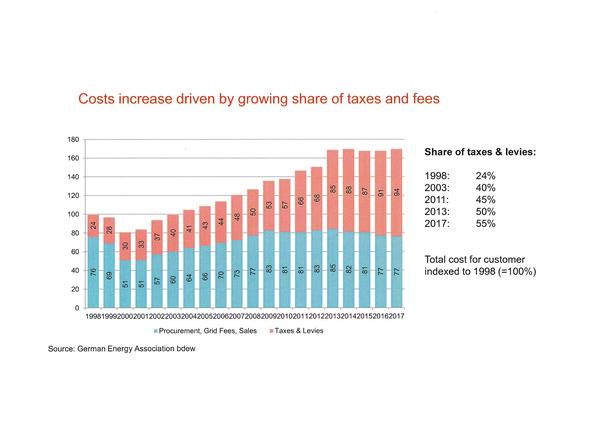

The state-induced proportion of contributions and taxes in the domestic electricity price of 29 €Cent amounts to 16 €Cent, thus constituting over 50% of the total price. The EEG levy alone amounts to almost 7 €Cent per kWh, and the tendency is for it to increase further (see chart 6).

Special attention also has to be given to the network charge, which nowadays amounts to 7.5 €Cent per kWh, but on account of the tremendous development of the network, the storage and system costs are also set to increase in future. Thus in 2015 the re-dispatch costs alone amounted to approximately one billion euros, also with a rising trend. I would like to explain these costs briefly because they represent good evidence of the irrationality of the German energy policy.

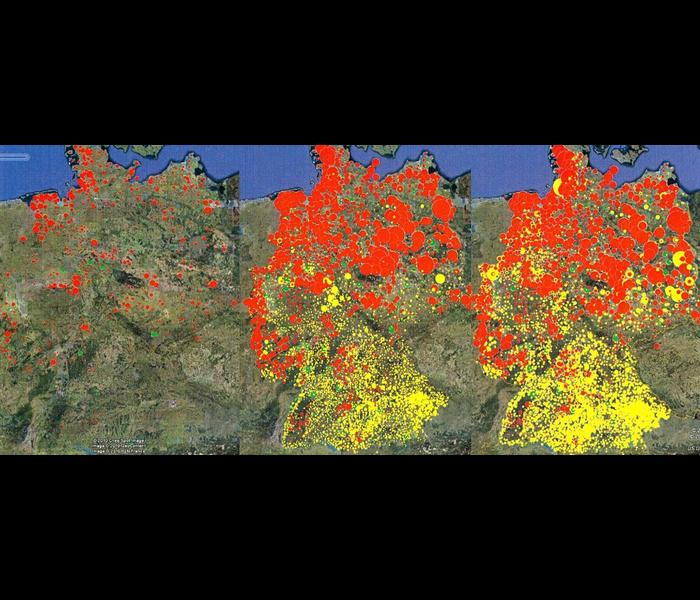

On account of the tremendous development of wind energy in the north of Germany, as well as offshore in the North Sea and Baltic Sea (chart 1) considerable additional grid capacities are required at maximum voltage level, in order to transport the electricity from the regional states in the north where demand is low, to the more industrialised states in the west and south where demand is higher. This much-needed extension of the grid, however, meets with great resistance amongst the population. In turn this leads to serious delays in the development and consequently to the fact that full scale transportation of the available power is not possible. Therefore wind farms have to be regulated when the wind is particularly strong. Electricity which is not generated nevertheless has to be paid for because the operator is entitled to statutory remuneration via the EEG.

At the same time, in the south of Germany and in other European countries, e.g. Austria, Italy and the Czech Republic, old fossil fuel fired power stations are being commissioned in order to serve the energy market and ensure that it continues to function. In 2016 these re-dispatch costs amounted to one billion euros. By 2020 the German Federal Network Agency expects costs of 4.5 billion euros. This situation is likely to continue for a long time because the grid capacities required today are not likely to be ready until after 2025 and in the north, meanwhile, wind farms continue to be built. This, in fact, is quite senseless, both in terms of energy policy and economic considerations. But it does not prevent the government from continuing nevertheless.

In the electricity sector the actual situation today may be described as follows:

• Demand in Germany fluctuates between 35 and 82 GW.

• Installed power station capacity amounts to 200 GW, of which approximately 90 GW comes from PV systems and wind farms, and is therefore not reliably secured.

With this over-sized but necessary power plant park it is possible - for now - to guarantee supplies. The situation will change, however, at the latest by 2022 when all German nuclear power stations are closed down. Particularly in Germany, this will lead to a shortage in capacity - amounting to as much as 5.5 GW of reliable power station capacity in Bavaria alone.

On account of the great insecurity on the energy market, the unpredictable political circumstances and the low energy exchange prices, no investors nowadays are willing to construct new power stations. The German government, however, in guaranteeing reliability of supply, is relying on the European electricity grid - which can indeed lead to some very bizarre results.

In a report issued by the German Federal Network Agency in 2014, it is ascertained that, in order to maintain the reliability of supply in southern Germany, it will be necessary to use electricity generated by Fessenheim nuclear power station in France. This seriously discredits the German energy transition. We are closing down state-of-the-art nuclear power stations in Germany - but need to resort to acquiring supplies from one of the oldest French nuclear power stations (which even the French would like to close down) in order to secure the necessary reliability.

At this point I would like to emphasise that the German energy transition is being implemented on a fairly solitary and isolated basis within Europe - a situation which leads to conflicts with our European neighbours in many cases. The interconnections to Poland, for example, have either been shut down, or their use is controlled by phase modifiers. The Poles no longer accept the increasing and uncontrolled transport of German wind energy via their grid, because this seriously restricted the operation of their own power stations. It is, therefore, no longer possible to speak in terms of a uniform and coordinated European energy policy, although this is urgently needed, because - also in France, Poland and other European countries - there are plans to close down many power stations over the next 15 years. In France, for example, the EDF plans to reduce the proportion of nuclear power from today's level of 75% to 50% by 2030. And yet the issue of which power stations are to provide a replacement, remains fairly open - particularly also with regard to the climate protection goals. And this gives me the cue to move on to the next major problem area in connection with German energy policy, climate protection policy.

Germany is not achieving its climate protection goals

On the topic of climate protection the German government is very committed at international level, as could be clearly observed recently at the Paris Climate Change Conference or at the G20 meeting in Hamburg. Very ambitious climate protection goals for Germany are defined by the government. These will not be achieved, however - let me say this right away, to get straight to the point. In Germany it is intended for the CO2 emissions to be reduced by 40% vis à vis 1990 by 2020, and by 80-95% by 2050, which means complete decarbonisation. But what is our position today?

It can be ascertained that, despite massive efforts, the CO2 emissions in Germany have not been reduced over recent years - on the contrary, there has been a slight increase. The reasons for this are that in the electricity system, on account of the merit order regulation, the lignite and coal fired power stations have to remain in the system, which also makes sense with regard to costs. The existing natural gas fired power stations are being dispelled from the system on account of the massive expansion of electricity generated from renewable sources. In the traffic sector we have been able to observe increasing CO2 emissions over recent years, rather than the reduction which is required. Also in the area of energy saving or energy efficiency, we have not achieved the progress which we actually needed to. In particular the upgrading of buildings with regard to energy performance is not progressing at a sufficient rate. All analyses, therefore, come to the clear conclusion that we will not reach the 40% target by 2020.

In the last 27 years we have achieved a 27% reduction in CO2, and 18% of this reduction is a direct result of German re-unification and the closure of extremely inefficient power stations and industrial operations in the former Democratic Republic of Germany. It is impossible that within three years 13% of the CO2 emissions can be reduced, whilst at the same time phasing out nuclear energy.

The good news in this context is that, with its 2.7% proportion of worldwide CO2 emissions, Germany is fairly irrelevant for achieving the international climate protection goals. China, India, South America and Africa are the decisive countries as far as global climate protection is concerned. Both Germany and, of course, Japan are in a position as high-technology countries to supply the necessary innovations required for global climate and environmental protection, and can benefit from this economically.

The sobering development regarding climate protection has come about in spite of the fact that, ever since the year 2000, we have been investing enormous efforts in promoting the energy transition. We can ascertain that the energy transition is not an efficient strategy to reduce CO2 emissions, and is therefore also not a suitable instrument for climate protection. We currently spend an annual sum of 25 billion euros on generating electricity from renewable sources, and the trend is for this to increase. In the national energy efficiency action plan and in the climate protection plan 2020/2050 over 200 measures and instruments are defined, which are intended to contribute to an increase in the energy efficiency and to the reduction of CO2 emissions, combined with a KFW funding programme worth several billions.

At this point I would also like to refer back to the, meanwhile counter-productive, effect of the EEG, the German Act governing renewable energy. In Germany over the last 17 years, photovoltaic systems and wind farms have been built to produce a quantity of 90 GW, without the necessary grid structure being created, or the efficient integration of the fluctuating generation of power being organised into the system. As I have already explained, we no longer sell certain energy, rather we pay the customers to purchase it. It could, therefore be assumed, that the responsible politicians who are aware of all this, could learn from the situation and adapt their direction accordingly. Unfortunately, however, this is not the case!

The complete decarbonisation of Germany, and from my point of view the related de-industrialisation of Germany, is being pursued relentlessly. The German government, for example, would like to achieve the CO2 reduction in the energy area by planning a full-scale electrification on the basis of photovoltaic and wind energy. For this purpose, the concept of the sector coupling has been invented which, with the help of power to heat, power to cool, power to gas and power to wheel, as well as by demand side management, can ensure the entire energy supply.

In order to help you understand the full dimensions of what this really means, I would like to mention a few figures. By means of this strategy, the power consumption would increase tremendously - the figures here fluctuate between 800 and 3,000 TWh, thus reflecting a wide range. If we take the lower figure of 800 TWh, this would mean that in 2050 we would require a capacity of 250 GW from photovoltaic systems as well as wind farms providing 200 GW onshore and 85 GW offshore. The integration of over 500 GW of fluctuating capacity, involving the structure of 90 GW power to gas systems and 140 GW electric heat pumps, illustrates the dimensions quite clearly.

The fact that this scenario cannot be implemented - either from a technical or an economic point of view - within just less than 30 years, does not require any further explanation. And a further problem will be the social acceptance, because people will not be prepared to accept the huge impact this will have on the landscape and nature. This strategy, however, would mean a complete reorganisation of the industrial structure in Germany, not only in the energy industry but also in the car industry.

In Germany German car construction occupies first place in the processing industry concerning employment, added value, in capital investments, in exports/imports and in direct investments as well as activities in innovation as well as research and development. The economic power of regional states such as Bavaria, Baden-Württemberg and Lower Saxony is significantly influenced by the car industry and its supplier industry, on which it is also dependent. A conversion of the combustion engine to electric mobility, which is assumed in all energy transition scenarios, would completely restructure this sector of industry, with significantly negative results on the job market. This loss of jobs can not be compensated for, not even by the production of PV and wind farms. The PV industry provides clear evidence of this.

Whereas just a few years ago, the PV industry was regarded as the German industry of the future, combined with the hope of creating hundreds of thousands of jobs, the very sobering result is that now the German PV industry is virtually extinct. The last large PV manufacturer, Solarworld AG, was forced to file for bankruptcy this year.

As efforts undertaken so far to ensure climate protection have not achieved the desired result, the call for a quick closure of lignite and bituminous coal -fired power stations is becoming constantly louder. In an appraisal which has not yet been published, it is stated that if we are to achieve the 95% CO2 target by 2050, the German lignite-fired power stations have to be closed by 2030 at the latest.

The Green party have already included a call for this in their 2017 general election campaign. In such scenarios no consideration whatsoever is included either for the costs involved in the securing and renaturation of the open-cast lignite mines, nor who should be responsible for these, nor for the jobs which will be lost and the ensuing social acceptance. Such system-theoretical modelling mechanisms also do not investigate how with such scenarios Germany's competitiveness as an industrial location can be secured. Despite these assumptions, in the simulation models for 2050, the same industrial structure is still supposed, an absolute absurdity which destroys the credibility of all the scenarios. So you see, the situation remains as serious as it is complex.

I would not like to give rise to the impression that the energy transition and climate protection strategy in Germany is nothing less than a catastrophe. The three digit billion sum of money which, via the EEG, we have invested in promoting photovoltaic systems, is now benefiting the developing and emerging countries. In places such as Tajikistan, India or Africa, it is possible today with PV modules to product the KwH of power for less than three €cents. This makes it possible to make electricity available on a decentralised basis for pumping drinking water, for lighting and for computers in schools. The German mechanical engineering sector has also benefited from the boom of the PV industry in China, because 70% of the systems and machines with which PV modules are produced in China, in fact come from Germany. Also in Germany innovations in the energy field have gained a certain momentum which makes our country and our industry fitter for the future.

What I call for, however, is an end to the state-planned economy in which energy and climate policies are trapped today, so there are opportunities for more market economy and entrepreneurship. The demand for as much state as necessary, as much market as possible, remains correct and appropriate, and should once again be restored to the primacy of politics.

The implementation of the climate protection targets of Paris is not just an energy-related topic. It means a complete restructuring of our society, which can not be undertaken by one nation alone - it requires an international context. Also the energy transition, however, cannot be implemented simply by switching off the nuclear and fossil-fuel fired power stations, and commissioning photovoltaic systems and wind farms. Instead it requires an efficient optimisation of the system, involving all consumption and production sectors. And we still have a long way to go before we can achieve this.

Chart 1: Development of wind energy usage

Chart 1: Development of wind energy usage

Chart 2: Development of nuclear politics in Germany

Chart 2: Development of nuclear politics in Germany

Chart 3: Renewables generation

Chart 3: Renewables generation

Chart 4: Less & later for conventional generation projects

Chart 4: Less & later for conventional generation projects

Chart 5: Costs for consumers have increased

Chart 5: Costs for consumers have increased

Chart 6: Growing share of taxes and fees

Chart 6: Growing share of taxes and fees